NACH, or the National Automated Clearing House, was a system introduced by the National Payments Corporation of India, for interbank, high volume, electronic transfers, which were periodic in nature. The NPCI introduced NACH as an improvement over the existing Electronic Clearing System (ECS), and consolidate multiple ECS systems running all over the country. The NACH system is used for bulk towards the distribution of subsidies, dividends, interest, salary, pension, etc. and also for bulk transactions towards the collection of payments for telephone, electricity, water, loans, investments in mutual funds, insurance premium, etc.

NACH hopes to have a national reach, and bring together all core banking branches of its partner branches. It follows a common set of standards and rules and even includes support for Aadhaar based transactions. NACH also provides a high level of security and enables the partners to scale in a cost-effective manner. The amount of manual intervention has been reduced, with less paperwork and friction between institutions.

NACH also reduces the turn-around time for mandate activation from 30 days, in case of ECS, to around 10 days. The new Mandate Management System, creates a unified format for mandate across all its partner banks, maintaining the legacy registration process.

The Reserve Bank of India (RBI) has announced that the National Automated Clearing House (NACH) system will be available on all days, including Sundays and bank holidays, effective from August 1, 2021. This means that come August 1, your salary credit into your bank account, auto-debits related to mutual fund SIPs, home/car/personal loans EMI payments, bill payments such as telephone bills, gas payments, electricity bills etc. will take place even on bank holidays.

Comparing NACH to ECS

A few key points while comparing NACH to ECS:

- NACH is much faster with same day presentation, settlement and returns processing, compared to the ECS system, where the entire process spreads over 3 -4 days.

- NACH has a well defined Dispute Management System, to raise and solves issues, which was absent in the case of ECS.

- NACH also has a robust Mandate Management System, with standardised mandate format and verification workflow.

- NACH introduced the Unique Mandate Reference Number to clearly identify each mandate with reference to a customer.

How is NACH utilized by other institutions?

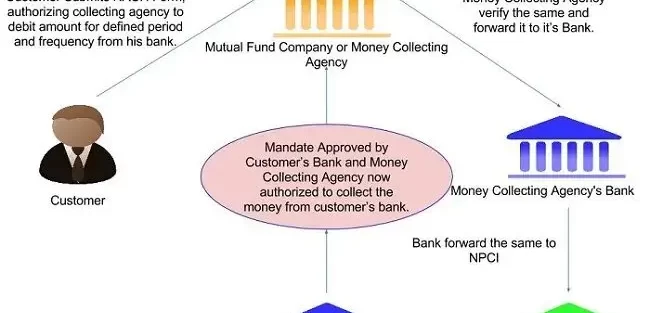

Suppose an individual borrows money from a lending institution and agrees to pay it off in equal monthly installments. The institution offers the individual two modes of repayment. Either by transferring the EMI amount directly to the account of the institution ( via bank account transfer, UPI, online wallets, etc.), or auto debiting from the individuals account on a fixed day of every month. To avail the option of auto-debit, the individual is asked to fill out a NACH Mandate form, authorizing the institution to debit the amount from their account. The institution then sends the mandate form to their bank (Sponsor Bank), which in turn sends it to the individual’s bank, via NPCI’s Mandate Management System.

The mandate is then verified at the individual’s bank, for matching account details and signature. Once it is approved, the individual is notified that the mandate has been activated, over the Phone, SMS or email. The Sponsor Bank is then provided with an approved mandate detail, which includes the UMRN.

The UMRN or the Unique Mandate Reference Number helps the sponsor bank, identify the individual and their bank. The sponsor bank then returns the mandate details with the UMRN to the institution, which is used by them during the auto-debit process.

Nach Mandate Form

A NACH Mandate is an authorization that an individual provides to an institution to credit or debit funds from their account. The mandate has a standardized format, as designed by the NPCI across all partner banks. A sample of the form is shown below:

There are two types of NACH mandates, Credit and Debit Type. The one shown in the image above is of Debit Type, ie. to debit funds from an individual’s account, which is the most common use case.

The Individual is required to provide the Bank Account Number, Bank Name and the IFSC or the MICR code, of the bank account, they wish the money to be deducted from.

The Frequency of the debit maybe Monthly, Quarterly, Half Yearly, Yearly or As and when presented. The ‘As and when presented’ option enables the institution to debit the amount on any date, and even multiple times a month. This gives the user the flexibility of the user to request the institution to postpone the debit in case of unavailability of funds in their account.

The mandate also provides a provision for specifying a Period, or the lifetime of the mandate. The From date specifies when the mandate is active from, and the To date specifies when it expires. The mandate also has a provision of extending the expiry until cancelled, which can be useful in case of recurring debits, like SIPs.

The Sponsor Bank Code and the Utility Code are filled by the institution issuing the mandate to the individual. These Utility Code helps uniquely identify the institution registered with NPCI and the Sponsor Bank Code identifies the Bank they are associated with.

Cancelling a NACH Mandate

Cancelling a NACH Mandate before its expiry can be done both by the institution and the individual. In case of the institution, a NACH mandate form, as the one shown above is submitted with the individual’s details, with the Cancel option ticked.

For the individual, cancelling can be done by approaching the bank directly, or via the net and mobile banking. Active mandates on each account are usually displayed under the NACH section of the Account/ Service related information.

E-NACH

With E-NACH payment service, you can now easily pay your loan EMIs from your bank account, without the need for paper based mandates. E-NACH stands for Electronic National Automated Clearing House.

All you need to do is, complete a one-time authentication for registration of the mandate with your Net Banking details or debit card, after which all subsequent payments will not require your intervention.

Benefits

- No need of cheque book/PDCs while availing loan facilities

- Simple and hassle-free process for collecting recurring payments

- Enhanced user experience as a result of error-free registration and payment automation

- Avoidance of late fees and penalties due to timely auto-debit of transaction amount

- 24 X 7 capability for mandate registration directly from website, no need to visit the branch

Process of Registration of ENACH

Individuals can automate their recurring payments of periodic nature using eNACH by integrating it into their existing system. The steps explained shows how to register eNACH to help a customer, who avails a secured loan like a home loan on a condition to repay in equated monthly instalments (EMI).

Step 1: Check if you are eligible for eNACH

You are eligible for eNACH registration if you have an active Internet banking facility or debit card of a particular bank, which accepts net banking, as well as a debit card as a payment method. If you do not have it, you can apply for the same at the nearest branch of that specific bank.

Step 2: Initiating eMandate

For initiating eMandate, you have to contact your bank either in person or over phone. The customer service representative at the bank will help you request for the eNACH registration by filling in the details such as the name of the account holder, email address or mobile number, start date and end date of EMI payment, amount type, frequency of payment, maximum amount to be debited, LAN (16-digit alpha numeric), customer bank account number, and name of the bank.

You should also confirm whether you want to opt for the EMI payment through net banking or debit card. The completed form is sent after authentication by your bank (the destination bank) to the sponsor bank.

Step 3: Receive an email and SMS

The next step in the eNACH registration process is receiving an email and SMS on your registered email address and mobile number requesting you to register for eNACH by clicking on the link provided. The link will be valid for 10 days.

Step 4: Verification and authentication by the customer

You will have to click on the link given to take you to the eNACH preview page. In case you have chosen the payment mode through net banking, you will find all the Mandate and generic details mentioned earlier, including your PAN number for verification. After verifying the details, you need to confirm it by clicking on the ‘Confirm’ tab. It will show you the bank authentication page confirming all the above details, including the bank name, account number and mandate amount.

Next, you have to confirm the details and verify the OTP sent to your registered mobile number. On registering for eNACH, a nominal amount will be debited from your account to confirm the registration. You will receive the transaction details confirming the eMandate.

The authentication process for the debit card is also similar, except that you need to verify the debit card number, PIN and expiry date provided. Finally, you will receive an acknowledgment for eNACH registration for the repayment of your loan.

Post Disclaimer

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxchanakya has exercised reasonable efforts to ensure the veracity of information/content published, Taxchanakya shall be under no liability in any manner whatsoever for incorrect information, if any.